Our spring term ended a few weeks ago. I teach an undergraduate course that focuses on the economic history of the twentieth century. Unsurprisingly, the Great Depression is a major focus. The current mainstream view is that monetary shocks were very important in causing the initial contraction in the United States, and that the Gold Standard (the system of fixed exchange rates) was the principal mechanism that transmitted these shocks around the world, turning an otherwise normal recession into a prolonged depression. Countries did not recover until they left gold and devalued, which reduced real wages, increased profitability, raised competitiveness, and lowered interest rates.

But what of Africa?

Africa in the Great Depression

The monetary story also seems to hold for Latin America. For Africa, however, the pattern was different. A year ago, one of the MPhil students in economic and social history found no relationship between export recovery and when the colonial power abandoned gold in a sample of African countries.

Indeed, Susan Martin has argued that the entire period between the wars was a long depression for Africa. For commodity producers, export prices had already declined before 1929. Influenced by images of the American dust bowl, colonial administrators intensified coercive efforts at soil conservation. The Second World War was not a reprieve either: for many Africans, the increased wartime demand for commodities was offset by government controls, rising import prices, conscription, and forced labour. Some of my own work has looked at the wartime transition in the rubber industry in Nigeria’s Benin region.

Africa in the Great Recession

A quick look at the World Development Indicators shows that, while African growth rates have slowed since 2007, they have not turned negative. African growth lags Asia, but remains stronger than in North America or the world as a whole. GDP per capita tells a similar story: African incomes have been growing more slowly since 2007, but did not fall on average. Africa has fared better during the Great Recession than during the Great Depression.

Why?

Jake Bright suggests a set of reasons for this: African growth, a growing consumer class, modernization of banking and telecommunications, and newly-created stock markets have attracted foreign investment, aided by remittances.

Antoinette Sayeh cautions that countries with export markets in advanced countries have had worse experiences with the depression, as have those still engaged in conflict. Her focus is on two factors: strong pre-recession growth (driven by commodity prices, debt relief, and market liberalization) and cushioning factors (high commodity prices, growth in other emerging markets, lack of financial crisis, and a lack of austerity).

Gareth Austin (whose other work I recommend) is also cautious. African growth has slowed, and Africans faced higher global food prices even before the recession. He suggests that richer African countries felt the recession first, due to their integration into world financial markets. Poorer countries have been hit by a fall in commodity prices. He does, however, suggest several influences that have cushioned the blow: strong pre-recession fiscal and trade balances due to previous structural adjustment, floating currencies, and early recovery in China and India. Can data help us sort through these explanations? The WDI and IMF World Outlook provide data on many of the variables mentioned above. In particular:

- The growth rate of PPP GDP-per capita from 2001 to 2006 measures pre-recession growth.

- Log PPP GDP-per capita in 2006 captures convergence.

- The change in foreign direct investment from 2006 to 2010 measures the resilience of foreign investment since the recession started.

- The change in the net barter terms of trade from 2006 to 2011 measures changes in the trade environment, including commodity prices, since the recession started.

- Central government debt as a fraction of GDP in 2006 measures the pre-recession fiscal position.

- The weighted mean tariff rate on all products in 2006 measures market liberalization before the recession.

- The CPIA financial sector rating in 2006 measures the strength of the financial sector before the recession.

- The change in the official exchange rate from 2006 to 2012 measures the extent of currency devaluation through the recession. This is reported in LCU per USD, so higher values correspond to a decline in the value of the local currency.

- The change in the government expenditure from 2006 to 2012 (deflated by the GDP deflator) proxies for the extent to which austerity has been avoided.

- Remittances received in 2006, per capita, are also available.

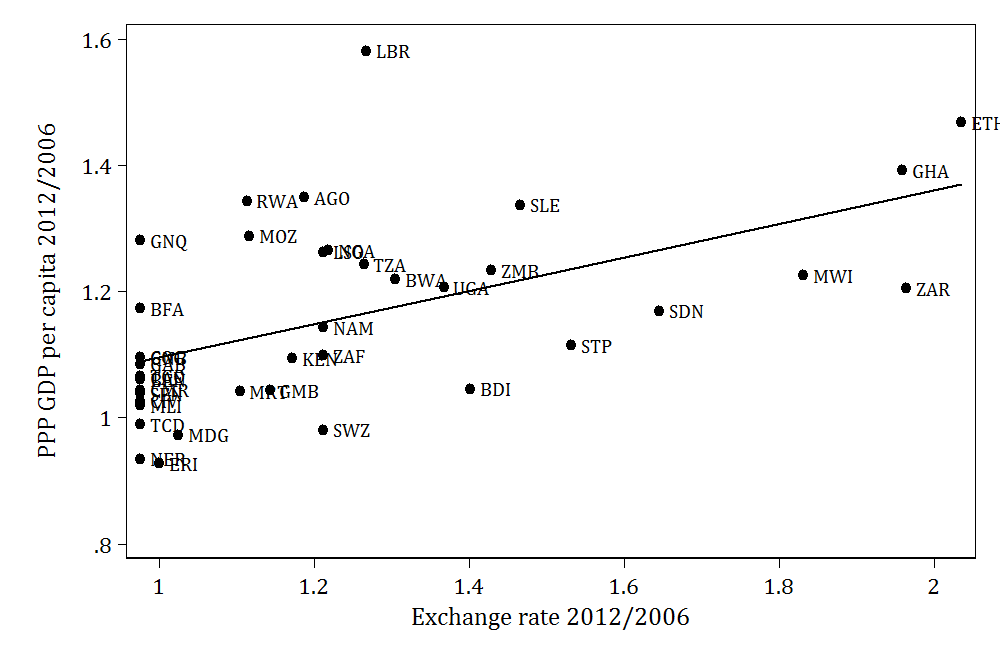

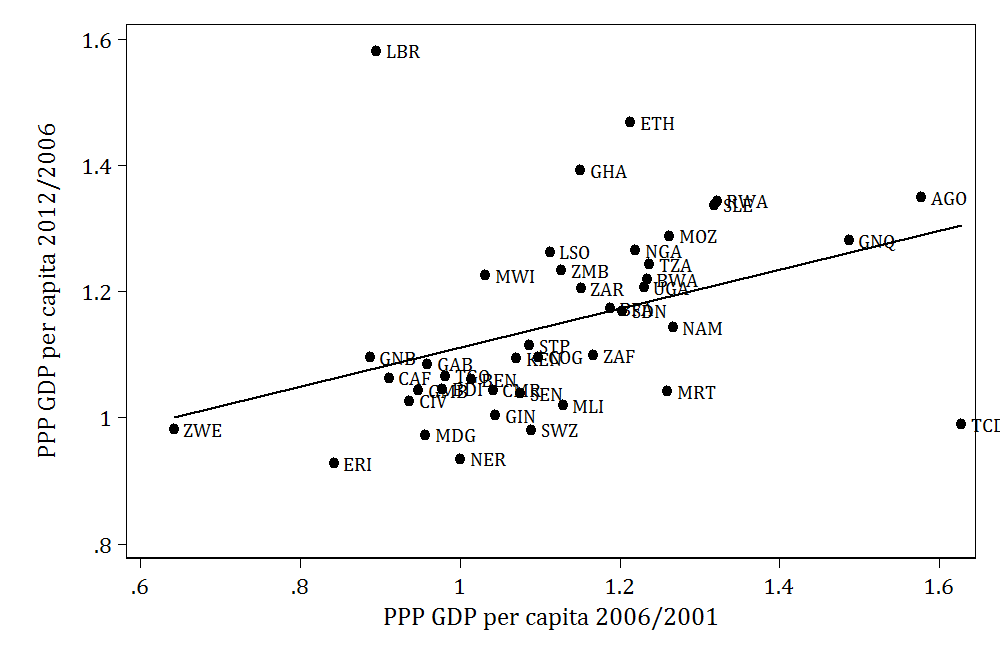

Are any of these correlated with relative growth performance between 2006 and 2012? I have posted some naive cross-country regressions below. These are neither careful nor causal, but the results are surprising. Only two variables stand out as predictors of growth through the recession: pre-recession growth, and exchange rate devaluation.

These correlations are large: I plot them below. A one standard deviation increase in pre-recession growth is correlated with of a 0.40 standard deviation increase in growth since 2006. A one standard deviation increase in the extent of devaluation (column 4) is correlated with a 0.53 standard deviation increase in growth since 2006.

Together, these tell an unusual story: the African countries that have fared well during the Great Recession are those that were doing well before it and those who have devalued their currencies.

You can have a look yourself: download the .do files and data (Stata) used to produce these graphs and tables here.